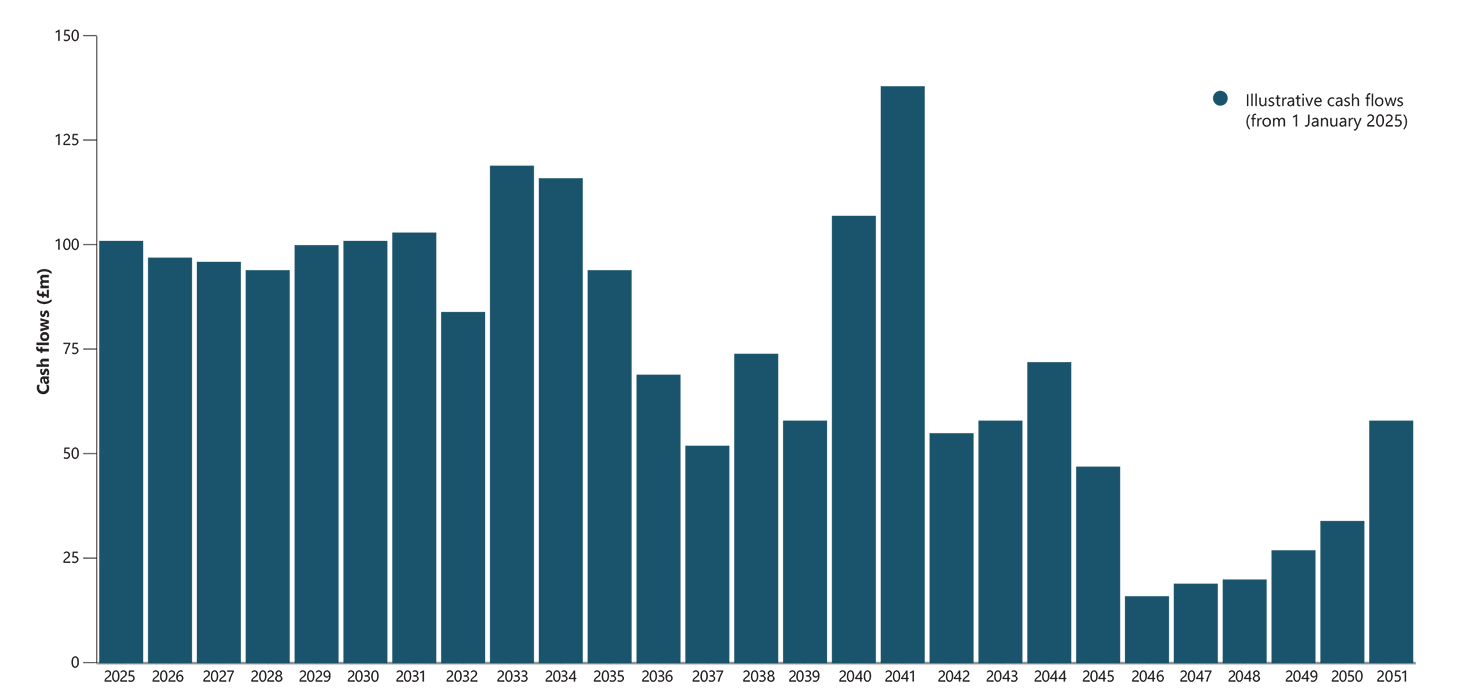

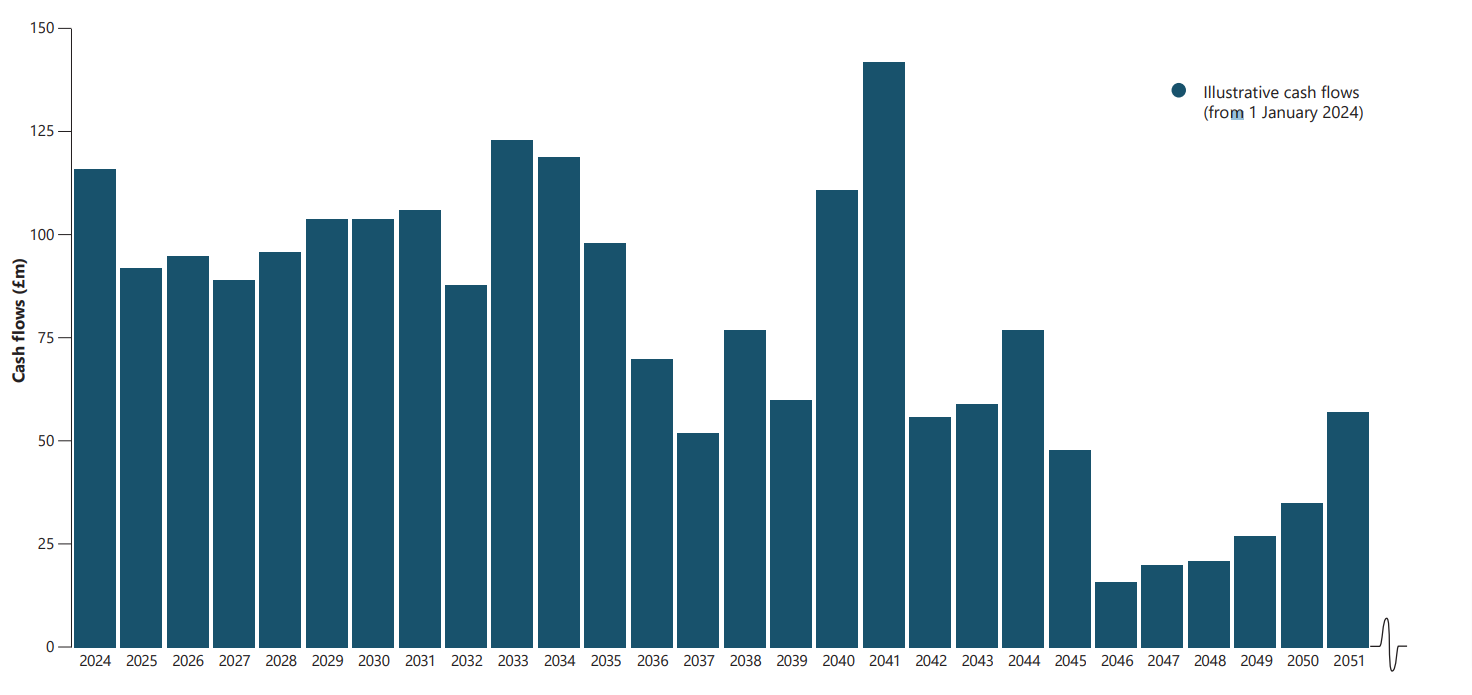

This illustrative chart, as at 31 December 2024, is a target only and is not a profit forecast. There can be no assurance that this target will be met. This chart reflects the target cash flows, including the cash generated in prior years that has yet to be distributed to the Company, at the reporting date. It also does not consider any further acquisitions, unforeseen costs or expenses, taxes incurred within the Company structure, or other factors that may affect the portfolio assets, and therefore the impact on the cash flows to the Company. As such, the chart above should not in any way be construed as forecasting the actual cash flows from the portfolio. There are cash flows extending beyond 2051 but for illustrative purposes, these are excluded from the chart above.

The Company’s assets generate long-term cash flows from government or government-backed counterparties, ensuring high visibility and predictability. While concession-backed cash f lows are resilient, inflation-linked and defensive, they have a finite life, ending with each concession term.

Concession assets make up 94% of BBGI’s portfolio, with the remaining 6% comprising non-concession assets. Unlike concession arrangements, where assets return to the public client at the end of the contract, nonconcession assets are freehold or long-term leasehold interests. This category includes a portion of BBGI’s UK Local Improvement Finance Trust (‘LIFT’) assets such as primary healthcare facilities, which are designed for long-term use. With regular maintenance and upgrades, these assets can achieve significant long-term income-generating lifespans.